PICTURES ARE LOADING...

Reference:

EDEN-T85795102

/ 85795102

Reference:

EDEN-T85795102

Country:

ES

City:

Arrecife

Postal code:

35500

Category:

Commercial

Listing type:

For sale

Property type:

Business opportunity

Property size:

560 sqft

REAL ESTATE PRICE PER SQFT IN NEARBY CITIES

| City |

Avg price per sqft house |

Avg price per sqft apartment |

|---|---|---|

| La Oliva | USD 196 | - |

| Puerto del Rosario | USD 165 | USD 146 |

| Fuerteventura | USD 169 | - |

| Las Palmas | USD 186 | USD 236 |

| Telde | - | USD 166 |

| Mogán | - | USD 333 |

| Santa Cruz de Tenerife | USD 231 | USD 262 |

| Tacoronte | USD 146 | - |

| Granadilla de Abona | USD 211 | USD 181 |

| San Miguel de Abona | USD 221 | USD 214 |

| Arona | USD 259 | USD 299 |

| Adeje | USD 321 | USD 297 |

| Guía de Isora | USD 205 | USD 284 |

| Santiago del Teide | - | USD 262 |

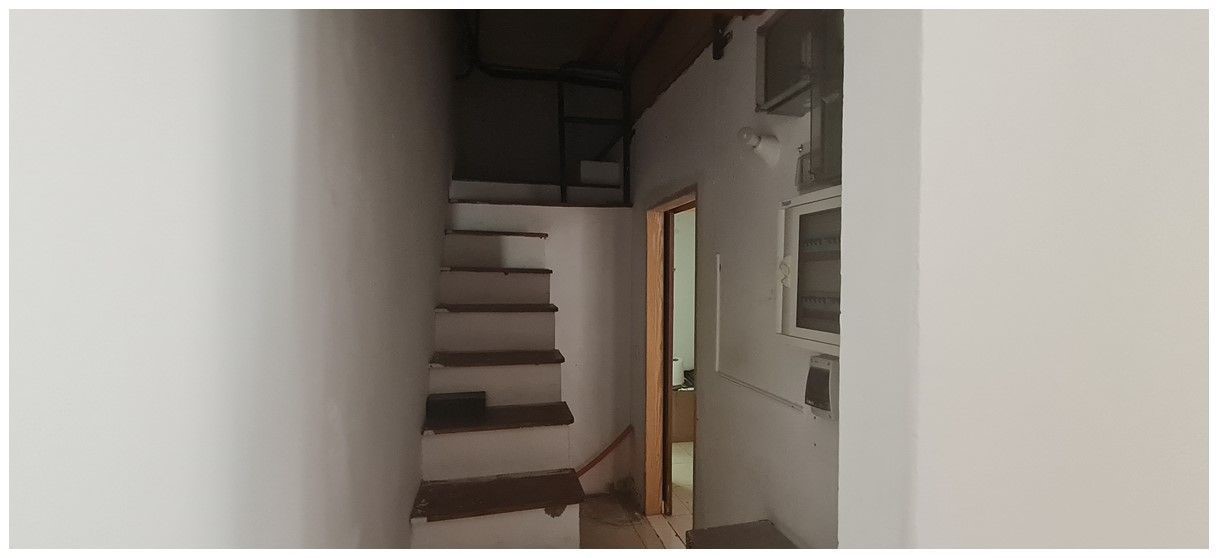

For more information contact us without obligation.Tax, notary and registration expenses are not included in the price.They do not require energy certification, since they are covered by article 5 paragraph 2 of RD 235/2013. View more View less Local comercial situado en la emblemática calle de León y Castillo, a escasos metros del Charco de San Ginés. Zona de gran afluencia turística y local.Tiene una superficie útil de 49 m2 y se distribuye en amplia estancia principal, altillo, un office y un aseo.Gran oportunidad para inversores o emprendedores.

Para más información contáctenos sin compromiso.Los gastos de impuestos, notaría y registro no están incluidos en el precio.No precisan la certificación energética, ya que se acogen al artículo 5 apartado 2 del RD 235/2013. Commercial premises located in the emblematic street of León y Castillo, a few meters from the Charco de San Ginés. Area of great tourist and local influx.It has a useful area of 49 m2 and is distributed in large main room, loft, an office and a toilet.Great opportunity for investors or entrepreneurs.

For more information contact us without obligation.Tax, notary and registration expenses are not included in the price.They do not require energy certification, since they are covered by article 5 paragraph 2 of RD 235/2013.